Build a Data Strategy for Property & Casualty Insurance

Turn fragmented insurance data into reliable, actionable insights.

- Data is fragmented across policy, claims, actuarial, and financial systems, limiting trust and usability.

- Inconsistent definitions and unclear ownership weaken pricing, reserving, reporting, and model governance.

- Manual reconciliation slows analysis and increases operational risk.

- Regulatory expectations demand stronger transparency, explainability, and documentation.

Our Advice

Critical Insight

Reliable and well-governed data strengthens pricing, claims accuracy, reserving confidence, and audit readiness, creating a real competitive advantage for P&C insurers.

Impact and Result

- Improved data quality, consistency, and integration across underwriting, claims, and actuarial workflows.

- Faster, more reliable risk and loss insights to support pricing and reserving decisions.

- Stronger regulatory compliance, audit readiness, and measurable business value from data investments.

INFO~TECH RESEARCH GROUP

Build a Data Strategy for Property & Casualty Insurance

Turn fragmented insurance data into reliable, actionable insights.

Analyst perspective

The case for a stronger data strategy in property and casualty (P&C) insurance.

Insurance leaders are working in a landscape shaped by rising catastrophe losses, social inflation, and strict regulatory expectations. These pressures require decisions that are transparent, consistent, and grounded in accurate data. Yet many carriers still rely on information that is scattered across policy, claims, actuarial, and financial systems. Definitions often differ from team to team, and many processes depend on manual reconciliation. This creates uncertainty in pricing, increases claims leakage, affects reserve stability, and makes regulatory reporting difficult.

Across the industry, one theme is clear: Technology alone cannot solve these challenges. Meaningful progress is made when data is treated as a business asset with clear ownership, shared definitions, and structured stewardship. When quality checks, lineage, and documentation are built into everyday work in underwriting, claims, and actuarial analysis, insurers gain stronger accuracy, better transparency, and greater trust in their data.

This blueprint provides a practical approach for building that foundation. It brings together governance, data products, and modern platforms in a way that supports real business outcomes. These outcomes include improved pricing discipline, fewer data-related errors in claims, more reliable reserving, and stronger preparation for audits and regulatory reviews. By connecting data strategy to daily insurance work, carriers can turn scattered information into dependable insight that supports long-term financial and operational strength.

Vidhi Trivedi

Senior Research Analyst, Insurance

Info-Tech Research Group

Build a Data Strategy for Property & Casualty Insurance

Turn fragmented insurance data into reliable, actionable insights.

EXECUTIVE BRIEF

Executive summary

Your Challenge

P&C insurers face rising pressure to improve underwriting accuracy, reduce claims leakage, and meet stricter regulatory expectations.

Data remains fragmented across policy, claims, actuarial, and financial systems, making it hard to trust and use effectively.

Inconsistent definitions and unclear ownership limit confidence in pricing, reserving, reporting, and model governance.

Insurers need a clear data strategy that strengthens data quality, ownership, and governance across core business functions.

Common Obstacles

Data is scattered across legacy systems, spreadsheets, and siloed workflows, preventing a unified view of risk and loss.

Definitions for key elements such as loss cause, severity, exposure bases, and rating inputs vary across teams and jurisdictions.

Manual reconciliation slows analysis and increases errors.

Regulatory expectations for fairness, explainability, and documentation continue to grow.

These obstacles persist as many insurers rely on technology upgrades alone, without building the governance, stewardship, and processes required to sustain high-quality, reliable data.

Info-Tech's Approach

Info-Tech provides a practical guide for building a governed data foundation tailored to P&C needs.

The approach includes a readiness assessment, P&C governance framework, clear ownership roles, and standardized definitions.

A structured plan drives quick improvements in data quality, documentation, and integration.

Governance practices are embedded into daily underwriting, claims, and actuarial workflows to ensure lasting impact.

By aligning governance and data practices with business goals, insurers can turn fragmented data into reliable insight and measurable value.

Info-Tech Insight

Reliable and well-governed data strengthens pricing, claims accuracy, reserving confidence, and audit readiness, creating a real competitive advantage for P&C insurers.

Your challenge

A modern data strategy is difficult to achieve when insurers lack the foundation needed to support accurate, transparent, and trusted decisions.

This research is designed to help organizations who are facing these challenges:

- Data is fragmented across policy, claims, actuarial, and financial systems. Critical information is stored in multiple platforms, spreadsheets, and manual workflows, making it difficult to establish a single, trusted view of risk, loss, and exposure.

- Key insurance data elements lack consistent definitions and ownership. Loss cause codes, severity categories, exposure bases, and rating inputs are defined differently across teams and jurisdictions, limiting confidence in pricing, reserving, reporting, and model governance.

- Manual reconciliation slows decision-making and increases errors. Underwriting, claims, and actuarial teams spend significant time correcting mismatched data, rebuilding lineage, and validating inputs to satisfy regulatory expectations for fairness, explainability, and audit readiness.

P&C insurers spend over US$23 billion each year on defense and cost containment due to rising litigation and bodily injury claim severity. (Ernst & Young, n.d.)

Rising litigation and injury severity, which cost P&C insurers more than US$23 billion a year, show why insurers need cleaner, more consistent, and better governed data.

- Inconsistent claims data fuels disputes and increases defense costs.

- Fragmented systems slow investigations and lengthen litigation.

- Varying severity and exposure definitions distort reserves.

- Weak lineage reduces explainability during audits and reviews.

- Manual data cleanup delays decisions and increases claim severity.

Common obstacles

Current data environments make it difficult for insurers to build a trusted, analytics-ready foundation.

These barriers make this challenge difficult to address for many organizations:

- Data lives in disconnected systems that do not speak to one another. Policy, claims, actuarial, and financial data are stored in separate platforms, spreadsheets, and third-party feeds, preventing a unified view of risk and loss.

- Definitions for critical P&C data elements are inconsistent. Loss cause codes, severity categories, exposure bases, and rating inputs vary across teams and jurisdictions, reducing confidence in pricing, reserving, and regulatory reporting.

- Lineage and documentation are incomplete or missing. Insurers often lack visibility into how data moves between policy administration systems (PAS), claims systems, actuarial models, and financial tools, making audit readiness and explainability difficult.

- Manual reconciliation consumes time and increases errors. Teams spend hours cleaning and validating data before it can be used for underwriting decisions, reserve analysis, or model governance.

- Technology investments alone do not solve data problems. New platforms fail to deliver value when governance, ownership, and stewardship roles are unclear, causing persistent quality issues and low adoption of analytics and AI.

Info-Tech’s approach

A structured methodology that strengthens data governance, ownership, and quality helps insurers build a trusted and analytics-ready foundation.

How Info-Tech helps insurers make progress:

- Assess data readiness to reveal gaps that affect underwriting, claims, and actuarial work. A P&C-focused assessment identifies fragmentation, inconsistent definitions, missing lineage, and quality issues that limit reliable decision-making.

- Design a P&C data governance framework with clear ownership and stewardship. Info-Tech provides defined roles, standardized data definitions, decision workflows, and policies that support auditability, transparency, and regulatory expectations.

- Launch a focused action plan that improves data quality quickly. A prioritized 90-day roadmap accelerates improvements in documentation, integration, and business-critical data elements such as loss coding, exposure bases, and rating inputs.

- Embed governance into daily processes to ensure sustained impact. Data practices are integrated into underwriting, claims, actuarial, and finance workflows so improvements become part of how work is done, not a separate initiative.

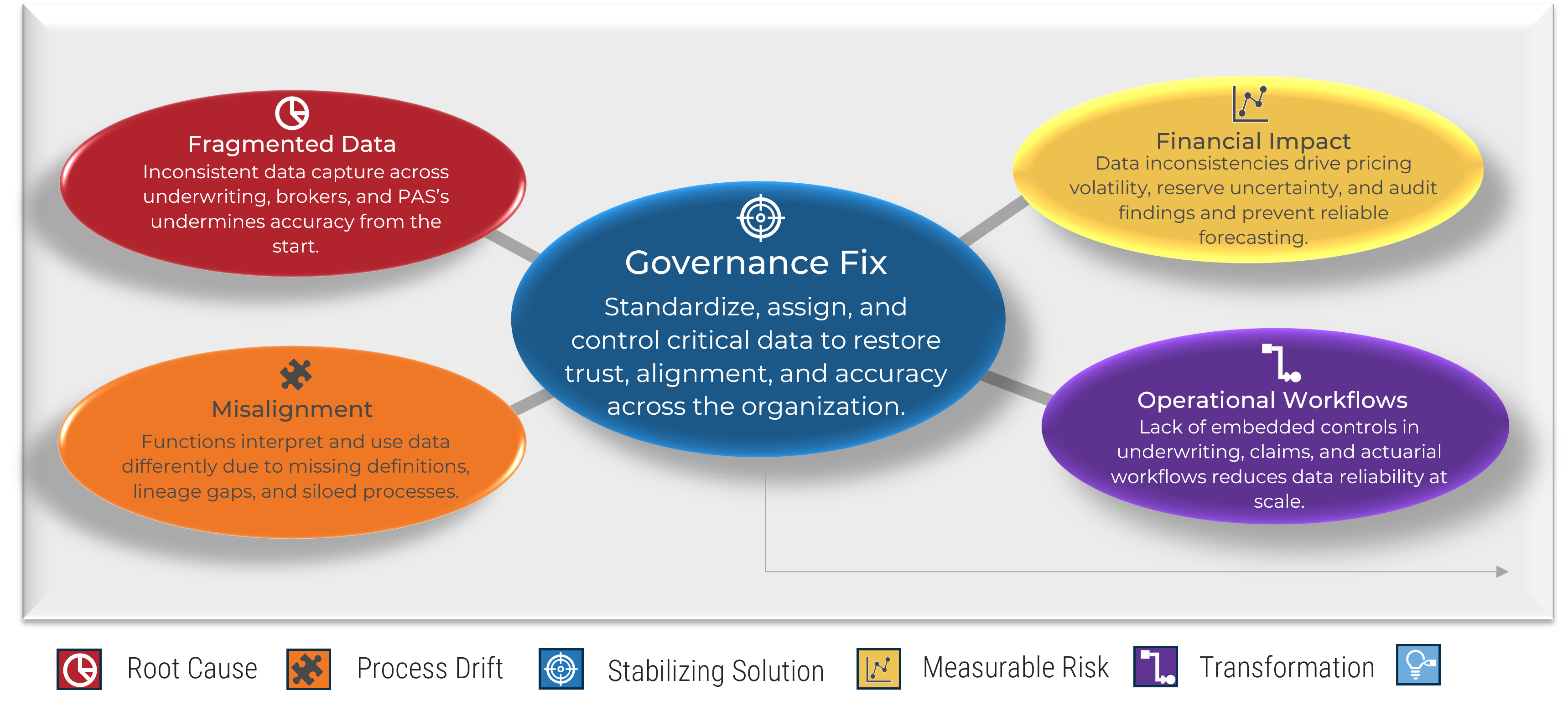

Rebuilding the insurance data value and reliability chain

How fragmented core data creates financial risk and governance restores confidence

Info-Tech’s Approach

Info-Tech helps insurers turn fragmented P&C data into a reliable, governed, and high-value business asset.

Info-Tech’s structured approach uncovers where inconsistent underwriting, claims, actuarial, and financial data create pricing uncertainty, reserve volatility, and leakage. Info-Tech then helps insurers standardize definitions, assign clear ownership, and embed quality controls that strengthen confidence in every decision.

Resilient Outcomes

Resilient Outcomes

The result of the full data reliability chain

- Strengthens pricing, reserving, and financial reporting accuracy.

- Reduces volatility caused by fragmented and inconsistent data.

- Embeds quality controls across underwriting, claims, and actuarial workflows.

- Increases trust, alignment, and confidence in core insurance data.

- Improves regulatory readiness and operational reliability.

Blueprint deliverables

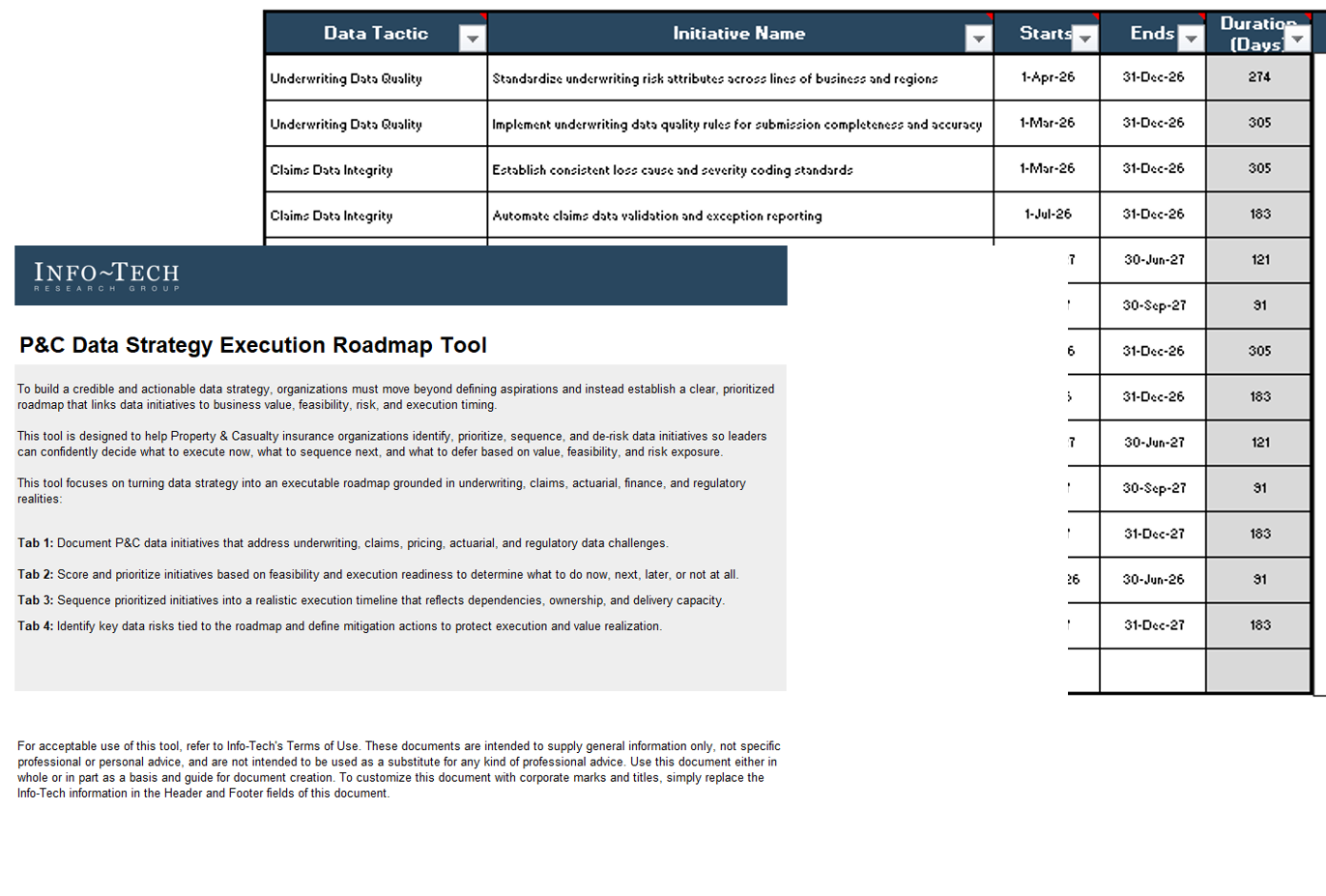

Key deliverable:

Data Strategy Execution Roadmap Tool

This tool helps P&C insurers prioritize, sequence, and manage risk across data initiatives to build a realistic, execution-ready data strategy roadmap.

Each step of this blueprint is accompanied by supporting deliverables to help you accomplish your goals:

Data Strategy Accelerator Tool

This tool helps P&C insurers assess data readiness and build practical data governance for core insurance outcomes.

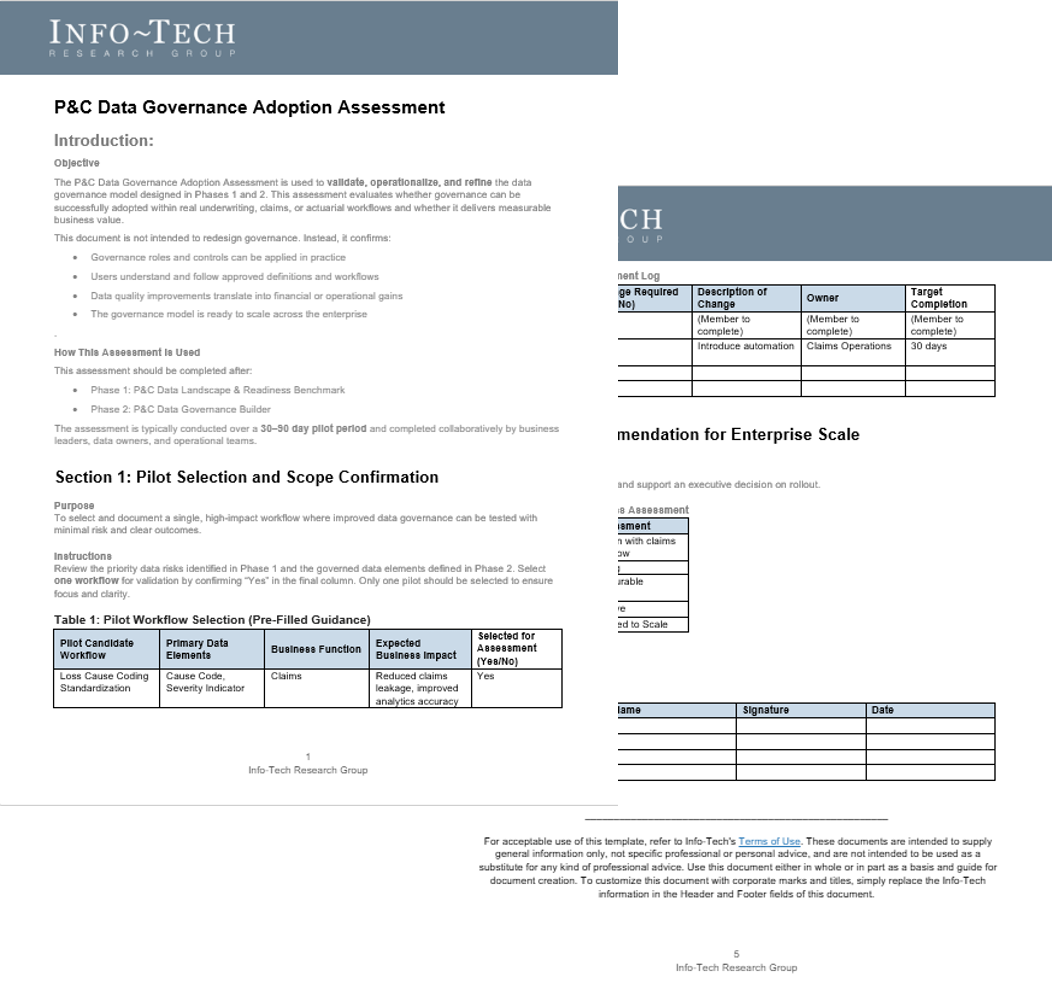

Data Governance Adoption Assessment

This assessment validates whether the P&C data governance model can be applied in real workflows and deliver measurable business and data quality outcomes.

Info-Tech’s methodology to build a reliable P&C data strategy

1. Assess the P&C Data Landscape and Readiness |

2. Design the P&C Data Governance Framework |

3. Pilot and Validate the Governance Model |

4. Build the Data Readiness Action Plan and Roadmap |

|

Phase Steps |

1.1 Create data vision and mission statements. 1.2 Establish P&C data scope. 1.3 Score P&C data readiness using the benchmark. 1.4 Translate findings into governance priorities. |

2.1 Identify and confirm critical P&C data elements. 2.2 Standardize data types for critical data elements. 2.3 Assign data ownership and stewardship. 2.4 Define governance controls and execution cadence. |

3.1 Select and scope a high-impact P&C workflow. 3.2 Apply governance model to the pilot workflow. 3.3 Enable users and measure pilot impact. 3.4 Capture feedback and refine the governance model. |

4.1 Assess data initiative feasibility. 4.2 Prioritize and sequence initiatives. 4.3 Build the execution roadmap. 4.4 Identify and manage strategic data risks. |

Deliverables |

|

|

|

|

Phase Outcomes |

|

|

|

|

Insight summary

Overarching insight

Treating data as a governed business asset, owned by underwriting, claims, actuarial, and finance teams, is the only way to turn fragmented P&C data into reliable insight and measurable business value.

Determine the P&C data landscape

Insurers often overlook how fragmented systems, legacy PAS setups, inconsistent broker feeds, and siloed claims processes distort key data elements such as loss cause, severity, exposure bases, and rating inputs.

Mapping the landscape reveals how these inconsistencies create reserve volatility, underwriting blind spots, and regulatory/litigation risk while limiting trust in analytics.

Design the governance framework

Governance brings stability by defining shared business terms, assigning ownership across underwriting, claims, actuarial, and finance teams, and enforcing documentation, lineage, and quality checks.

A strong framework reduces model risk, improves pricing and reserving accuracy, and supports expectations for fairness, explainability, and consistent enterprise use.

Drive adoption through a pilot

Pilots focused on high-value data elements, such as exposure bases or loss coding, show the immediate benefits of governed, high-quality data.

Reduced reconciliation time, improved reporting accuracy, and fewer definition disputes build confidence and create momentum for broader adoption.

Tactical insight

Manual reconciliation will continue to slow underwriting, claims, and reserving work unless insurers enforce data quality controls and lineage documentation at the source.

Tactical insight

Early focus on high-value elements like exposure bases, severity categories, and rating inputs produces faster business impact and reduces leakage and reserve volatility.

Project benefits

IT Benefits

- Improved data quality and consistency across systems. Reduces rework, integration issues, and mismatched inputs between PAS, claims, actuarial, and financial platforms.

- Clear governance roles and stewardship structures. Supports better ownership of data elements such as loss cause, severity, exposure bases, and rating inputs.

- Faster integration and analytics readiness. Governed and standardized data supports smoother platform modernization, model deployment, and regulatory reporting.

- Reduced manual reconciliation workload. Automation and quality controls decrease time spent cleaning and validating datasets across environments.

Business Benefits

- Stronger pricing and reserving accuracy. Consistent definitions and trusted data improve underwriting insight, reserve stability, and financial performance.

- Lower claims leakage and dispute risk. High-quality loss and exposure data reduces errors, litigation disputes, and downstream defense costs.

- Greater regulatory and audit readiness. Documented lineage, standardized definitions, and governance workflows support fairness, explainability, and compliance.

- Faster decision-making across underwriting, claims, and actuarial teams. Reliable data increases confidence in reports, models, and operational decisions, enabling better portfolio management.

Measure the value of this project

Build the data foundation that moves your organization from reacting to risk to leading with insight.

Consider tracking the following measures to demonstrate the value of a stronger P&C data strategy.

Metric |

Expected Improvement |

| Data quality scores (critical data elements) | Fewer errors and inconsistencies in loss cause, severity, exposure bases, and rating inputs, resulting in more accurate pricing and reserving. |

| Time spent on manual reconciliation | Significant reduction in effort required to rebuild lineage, validate inputs, and correct mismatched values across policy, claims, actuarial, and finance systems. |

| Underwriting and claims decision cycle time | Improved speed and confidence in decisions as teams rely on consistent, trusted, and standardized data rather than cleaning and reconciling datasets. |

| Regulatory and audit findings related to data | Fewer documentation gaps and exceptions as governance, definitions, and lineage practices strengthen audit readiness and compliance. |

| Accuracy of actuarial and financial reporting | More stable reserves, fewer late adjustments, and higher confidence in financial projections due to cleaner and better-governed data. |

| Analytics and model adoption rate | Higher usage of predictive models and analytics once data is standardized, governed, and supported by clear ownership and quality controls. |

Info-Tech offers various levels of support to best suit your needs

DIY Toolkit |

Guided Implementation |

Workshop |

Executive & Technical Counseling |

Consulting |

| "Our team has already made this critical project a priority, and we have the time and capability, but some guidance along the way would be helpful." | "Our team knows that we need to fix a process, but we need assistance to determine where to focus. Some check-ins along the way would help keep us on track." | "We need to hit the ground running and get this project kicked off immediately. Our team has the ability to take this over once we get a framework and strategy in place." | "Our team and processes are maturing; however, to expedite the journey we'll need a seasoned practitioner to coach and validate approaches, deliverables, and opportunities." | "Our team does not have the time or the knowledge to take this project on. We need assistance through the entirety of this project." |

Diagnostics and consistent frameworks are used throughout all five options |

||||

Guided Implementation

A Guided Implementation (GI) is a series of calls with an Info-Tech analyst to help implement our best practices in your organization.

A typical GI is 8 to 12 calls over the course of 4 to 6 months.

What does a typical GI on this topic look like?

Phase 1 |

Phase 2 |

Phase 3 |

Phase 4 |

| Call #1: Align on goals, scope, and current data challenges.

Call #2: Review data flows, inconsistencies, and business impacts. |

Call #3: Define ownership, stewardship roles, and shared definitions.

Call #4: Establish governance controls, workflows, and decision paths. |

Call #5: Select the pilot workflow and train users on definitions and rules.

Call #6: Measure pilot outcomes and refine the governance model. |

Call #7: Prioritize improvements and build the 90-day action plan.

Call #8: Finalize the execution roadmap and confirm next steps. |

Workshop overview

Contact your account representative for more information.

workshops@infotech.com 1-888-670-8889

Day 1 | Day 2 | Day 3 | Day 4 | Day 5 | |

Assess the P&C Data Landscape and Readiness | Design the P&C Data Governance Framework – Part 1 | Design the P&C Data Governance Framework – Part 2 | Pilot and Validate the Governance Model | Build the Data Readiness Action Plan and Roadmap | |

Activities |

|

|

|

|

|

Deliverables |

|

|

|

|

|

Build a Data Strategy for Property & Casualty Insurance

Phase 1

Assess the P&C Data Landscape and Readiness

Phase 11.1 Create data vision and mission statements. 1.2 Establish P&C data scope. 1.3 Score P&C data readiness using the benchmark. 1.4 Translate findings into governance priorities. | Phase 22.1 Identify and confirm critical P&C data elements. 2.2 Standardize definitions for critical data elements. 2.3 Assign data ownership and stewardship. 2.4 Define governance controls and execution cadence. | Phase 33.1 Select and scope a high-impact P&C workflow. 3.2 Apply governance model to the pilot workflow. 3.3 Enable users and measure pilot impact. 3.4 Capture feedback and refine the governance model. | Phase 44.1 Assess data initiative feasibility. 4.2 Prioritize and sequence initiatives. 4.3 Build the execution roadmap. 4.4 Identify and manage strategic data risks. |

This phase will walk you through the following activities:

- Clarifying what data matters most to the P&C business and why

- Gaining visibility into current data strengths, gaps, and constraints

- Understanding readiness across governance, roles, and enablement

- Establishing a focused set of data priorities to guide next steps

Align the organization around a shared P&C data strategy vision

A P&C data strategy should be an enterprise-wide capability.

- Creating a strong P&C data strategy vision requires active participation from underwriting, claims, actuarial, finance, compliance, and IT teams. A shared vision clearly defines how data supports pricing discipline, claims accuracy, reserving confidence, regulatory compliance, and analytics-driven decision-making.

- Once established, the vision must be consistently communicated across all functions involved in capturing, using, governing, and reporting insurance data. This ensures shared understanding of priorities, ownership, and expectations across lines of business and jurisdictions.

- The P&C data strategy vision should be reviewed and refined on a regular basis to reflect regulatory change, evolving risk profiles, new data sources, and modernization efforts across policy, claims, and actuarial systems.

Info-Tech Tips

- Use insights from underwriting, claims, actuarial, and regulatory stakeholders to anchor the data strategy in real insurance outcomes.

- Integrate cross-functional perspectives to ensure the strategy supports end-to-end insurance workflows rather than siloed functions.

- Define guiding principles that support trusted data, explainable models, and measurable business value across the P&C enterprise.

Define a clear vision and mission for your P&C data strategy

Vision: Where your P&C data strategy is headed

A vision describes how your organization intends to use data to operate and compete in the future.

A strong P&C data strategy vision aligns underwriting, claims, actuarial, finance, and IT around a shared outcome: trusted, governed data that improves risk selection, claims performance, reserving confidence, and regulatory credibility.

Your vision should be brief, clear, and aspirational, expressing how data will enable better decisions across lines of business and jurisdictions. It should reflect both business priorities and regulatory expectations and serve as a unifying anchor for all data-related initiatives.

Mission: Why your P&C data strategy exists

A mission defines the purpose of the P&C data strategy and how it delivers value today.

The mission should clearly state how the organization will deliver timely, high-quality, and well-governed data to support underwriting, claims operations, actuarial analysis, reporting, and analytics. It should reinforce accountability for data ownership, standardization, and controls that enable both operational execution and advanced analytics.

A strong mission provides a clear promise to internal stakeholders that data will be reliable, explainable, and fit for regulatory and business use.

Draft and align your P&C data strategy vision and mission

Vision and mission statements are crafted by workshop participants. These statements are to be reviewed, refined into a single version, approved by members of the senior leadership team, and then communicated to the wider organization.

Corporate (Reference Example)

- Vision:

Enable trusted, well-governed data as a strategic asset that strengthens risk selection, claims performance, reserving confidence, and regulatory credibility across the P&C enterprise. - Mission:

Foster an economic and financial environment conducive to sustainable economic growth and development.

Group 1

- Vision:

- Mission:

Group 2

- Vision:

- Mission:

{kind=link}

About Info-Tech

Info-Tech Research Group is the world’s fastest-growing information technology research and advisory company, proudly serving over 30,000 IT professionals.

We produce unbiased and highly relevant research to help CIOs and IT leaders make strategic, timely, and well-informed decisions. We partner closely with IT teams to provide everything they need, from actionable tools to analyst guidance, ensuring they deliver measurable results for their organizations.

What Is a Blueprint?

A blueprint is designed to be a roadmap, containing a methodology and the tools and templates you need to solve your IT problems.

Each blueprint can be accompanied by a Guided Implementation that provides you access to our world-class analysts to help you get through the project.

Need Extra Help?

Speak With An Analyst

Get the help you need in this 4-phase advisory process. You'll receive multiple touchpoints with our researchers, all included in your membership.

Guided Implementation 1: Assess the P&C Data Landscape and Readiness

- Call 1: Align on goals, scope, and current data challenges.

- Call 2: Review data flows, inconsistencies, and business impacts.

Guided Implementation 2: Design the P&C Data Governance Framework

- Call 1: Define ownership, stewardship roles, and shared definitions.

- Call 2: Establish governance controls, workflows, and decision paths.

Guided Implementation 3: Pilot and Validate the Governance Model

- Call 1: Select the pilot workflow and train users on definitions and rules.

- Call 2: Measure pilot outcomes and refine the governance model.

Guided Implementation 4: Build the Data Readiness Action Plan and Roadmap

- Call 1: Prioritize improvements and build the 90-day action plan.

- Call 2: Finalize the execution roadmap and confirm next steps.

Contributors

- Fahad Shaikh, Data & AI Advisor, Previously at Aviva

- Amanda Evenson, Vice President, Data & Analytics, Red River Mutual